The race to put computing infrastructure in orbit is accelerating as hyperscalers across cloud, AI, and space compete to see who will emerge winners in what many believe will fuel the Fourth Industrial Revolution.

The last few months have been a flurry of orbital data announcements, from SpaceX filing for a constellation of up to 1 million satellites to create an orbital data center and collaborating with AI giant Anthropic. Google is exploring Tensor Processing Unit (TPU) clusters in space. Starcloud has plans for an 88,000-satellite constellation aimed at delivering on-orbit compute at scale, to name a few.

Explore the June/July 2026 Issue

Check out more from this issue and find your next story to read.

In the face of this growing momentum, a single question dominates: Are orbital data centers a genuine paradigm shift — or the latest chapter in a long history of space industry hype?

The honest answer, based on conversations with industry leaders, including firms already flying hardware, is: it depends on who you ask, and what problem you think space can solve.

The Case for Getting Off the Ground

The push toward moving compute to orbit doesn’t emerge from a vacuum. AI is driving explosive growth in data center construction on Earth. U.S. spending on data center infrastructure jumped nearly 70 percent between May 2023 and May 2024, according to the American Edge Project. Energy consumption at those facilities could double or triple by 2028, accounting for up to 12 percent of U.S. electricity use, according to a report by Lawrence Berkeley National Laboratory. Communities from Virginia, Georgia, and Texas to Frankfurt, London, and Amsterdam are already pushing back against the land use, power draw, and water consumption that come with hyperscale campuses.

The pressure is severe enough that the industry is exploring radical alternatives — from servers on the seafloor to moving compute off the planet entirely.

“If you think about the three constraints for any data center, it’s land, it’s power, it’s water,” says Austin Litteral, director at Alpha Funds, a private investment firm focused on aerospace and emerging technology. “Space is rather vast, unlimited power via solar, and the water factor goes away when you think about cooling via radiator.”

Avi Shabtai, CEO of Ramon.Space — a company purpose-built to develop space-based computing infrastructure — frames the moment in even larger terms. “I think it’s the opportunity of the century,” he says, comparing it to the rise of cloud mega-infrastructure two decades ago.

Even with his optimism, Shabtai is candid about the technical and economic hurdles that must be cleared before massive orbital data centers can replace or supplement Earth-based facilities. Energy generation and storage, thermal management, radiation, transportation, and in-orbit maintenance all pose significant challenges.

“We’re dealing with a pretty hostile environment,” he notes, pointing to radiation and extreme temperature cycles, along with the need to cool systems efficiently in a vacuum.

Many enabling technologies exist today, but scaling them requires sustained engineering and, in some areas, true technological leaps. Ramon.Space is responding by developing space-based data center infrastructure, drawing on the company’s radiation-resilient processing, storage, and connectivity platforms built for the extreme conditions of space. It’s also formed a strategic partnership with manufacturer Ingrasys, a subsidiary of Foxconn Technology Group, to produce orbital data centers at scale.

James Mason, chief space officer at Planet, sees orbital data centers as a natural evolution of the EO company’s identity as a space and AI company that images Earth’s landmass every day to make global changes visible, accessible, and actionable.

“We’re essentially at the demo stage already,” says Mason, pointing to Planet flying Nvidia GPUs on on Pelican satellites to enable on-orbit AI processing. Planet and Google are also collaborating on early-stage orbital data center experiments that combine Google’s hyperscale cloud expertise with Planet’s heritage in small satellites and in‑orbit AI processing.

Planet has partnered with Google on a phased orbital compute demonstration set for early 2027, flying on Planet’s new Owl next-generation EO satellite constellation.

“This first phase is really about risk reduction for Google,” Mason says, noting that Google is funding the tests.

The program also funds higher-power satellite development that Planet wants for its core EO work — making it useful to both sides, regardless of how the orbital compute market develops.

“There’s no need for [new] physics here…so it is technically feasible. The challenge with orbital data centers are really power and thermal and doing that economically.”

Lower launch costs and better space traffic management will also be essential, he adds.

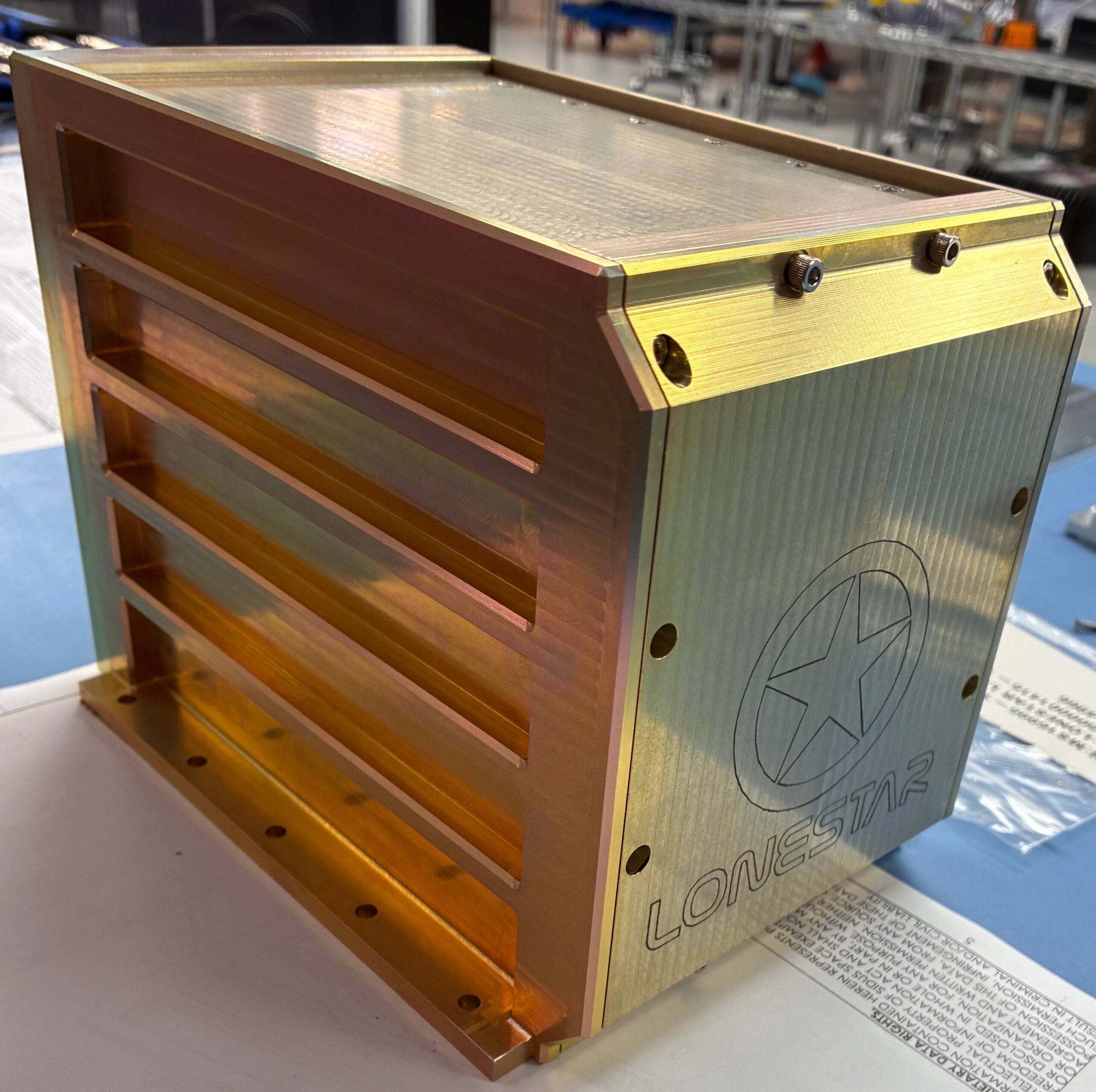

Another company, Lonestar Data Holdings, has flown four missions — two to the International Space Station and two to the lunar surface — to prove the feasibility of off-planet data storage. The Florida-based startup’s next commercial mission, a “Star Vault” satellite in polar orbit, launches in October with government customers already signed up.

“The constraints are just time and capital. The engineering is a known known,” says Chris Stott, founder and executive chairman.

He challenges the assumption that building in space is significantly more expensive than on the ground, pointing out that CapEx for data centers on Earth includes land acquisition and permitting, grid connections, power, cooling, and trenching for fiber, with projects often facing multi-year delays. In comparison, CapEx in space shifts to launch, spacecraft bus and payload, and space-qualified electronics.

“The rule of thumb is that the OpEx to run a modern data center for the first year is equal to the entire CapEx to build it,” says Stott, attributing the main expenses to power and cooling. By contrast, a space architecture drawing on solar power and radiative cooling could cut operational expenditure “by as much as 97 percent,” he says.

Building the Enabling Layer

While SpaceX and other big names chase constellation-scale ambitions, a quieter cohort of companies focuses on the hardware preconditions that must exist before any orbital data center becomes real. Luxembourg-based Edge Aerospace is one of them.

CEO Jaroslaw “JJ” Jaworski spent years at Made In Space and Redwire before co-founding Edge — experience that reinforced to him that big, orbital-scale visions only work if built on disciplined, incremental hardware gains.

“We didn’t want to build a company that targets something 10 to 15 years from now,” Jaworski says. “What we learned at Redwire was building products we could sell today and using recurring revenue to keep moving toward our North Star, which for us is orbital data centers.”

Jaworski and his co-founders spent nearly two years mapping what would have to happen — technically and economically — for orbital data centers to work, then built a product-first strategy around closing those gaps in sequence.

Edge is betting on low-SWaP computing systems and investing in hybrid onboard computers and network switches rather than chasing GPU-based space servers. Switching and networking, he argues, serve as the backbone of building servers in orbit — allowing modular scaling across connected nodes rather than cramming ever-more-powerful chips onto a single board.

In March, Edge launched its first demonstration mission as a hosted payload on SpaceX’s Transporter-16 rideshare mission. Edge’s in-orbit computing system successfully processed data directly in space, eliminating the need to send large raw datasets to Earth.

Only nine months after incorporation, Edge beat established primes to win a key European Space Agency study on orbital data centers. The ESA study reflects a use-case-first discipline that Jaworski sees as essential: rather than assuming orbital data centers are inevitable, it begins by asking whether real customers actually need them.

“Our job is to go to terrestrial data center companies and space companies and actually have real conversations: Do you need space data centers? What’s your real problem? Can we solve it with orbital infrastructure?”

Even the most enthusiastic proponents of orbital compute are careful about what they claim space can do. Stephen Eisele, president of Lonestar, argues that the near-term killer application isn’t AI training or general-purpose cloud compute. It’s storage.

“Storage is very low power. It takes up less than 15 percent of a typical data center’s power,” he says. “We don’t need to be on a monolithic structure. It’s going to be distributed over many satellites — and a big benefit there, of course, is for resiliency.”

Litteral at Alpha Funds holds a similar view. His firm’s interest in orbital compute began with edge compute — making satellites already on orbit smarter. That drew him to Sophia Space, a portfolio company developing a tile-based orbital computing platform that is solar-powered and passively cooled, optimized for AI inference at the edge.

“The near-term revenue opportunity is squarely in edge compute,” Litteral says, noting that full-scale, revenue-generating orbital data centers likely emerge in the late 2020s to early 2030s, scaling as launch prices fall and on-orbit manufacturing matures.

The Physics Problem No One is Talking About

Not everyone sees the path as clear. Brandon Karpf, a former U.S. Navy cryptologic warfare officer who leads international security partnerships at Japan-based NTT, a leading technology and communications provider and one of the largest data center operators globally, has analyzed five potential orbital compute business models: AI training, AI inference, public cloud, content distribution and edge compute, and sovereign cloud. His conclusion — only one model works: sovereign cloud.

“Sovereign cloud works because you’re not competing on the technology. You’re not competing with earth-based terrestrial-based compute…What you’re looking for is a strictly controlled regulatory regime that does not allow a foreign nation lawful intercept and lawful data collection,” explains Karpf, noting that the other scenarios fall short due to comms-bandwidth limitations.

He notes that today’s best optical satellite links deliver roughly 100 gigabits per second, with the next generation promising perhaps 400 Gbps. But Nvidia connects a single GPU into a training cluster at approximately 7.2 terabits per second — one to two orders of magnitude more than space links can provide, before accounting for the tens of thousands of GPUs that frontier AI training requires.

Karpf’s skepticism about AI training or public cloud in orbit isn’t opposition to orbital compute — it’s concern that capital-chasing GPU demonstrations on small test beds, rather than investing in communications infrastructure, could set the field back.

While current physics support AI inference, Karpf still sees it collapsing when customers experience delays introduced by a server orbiting hundreds of kilometers overhead. Public cloud fails on elasticity — the ability to scale resources up or down on demand — which Karpf says is extremely hard to reproduce with fixed, launch-constrained hardware in orbit.

The content delivery model in space isn’t cost-effective since content delivery network (CDN) workloads on Earth (which deliver video streams, images and static web content) require relatively low compute and storage and are hypercompetitive, which has pushed prices down. Putting these workloads into orbit adds launch and other costs that space can’t justify, especially when terrestrial CDNs are already embedded in thousands of points of presence close to users.

Data Sovereignty: The Use Case Everyone Agrees On

If there is one point of consensus across the skeptics and the believers, it is this: orbital storage for data sovereignty presents a compelling near-term business case in the sector.

Stott frames it in terms of a tightening global regulatory landscape. “It’s now illegal for you to send your data outside of the United States for processing and storage. It’s a federal crime,” he says. “One hundred and forty-one countries have the same kind of laws.” He notes that data infrastructure has also become a target of active conflict, citing recent attacks on cloud infrastructure in the Middle East.

Eisele draws out the implication for governments. A satellite-based storage vault, under established international space law, remains within a nation’s sovereign jurisdiction while being physically unreachable to any adversary on the ground.

“Imagine your country,” Eisele says, “and you can put your most important data in space. It’s out of reach of everyone, and it’s still, under established international law, part of your data sovereignty.”

Karpf sees it as the only defensible near-term business case, citing that sovereign cloud fetches the highest price per unit of compute of any data center business model.

Hype Cycle, or Great Profit Engine?

The framing of orbital data centers as a hype cycle is one that Stott finds familiar. “I’ve seen this happen two times before,” he says. “The first time was satellite broadcasting. Everyone at the time said it’s a hype cycle and then it turned into the most profitable use of satellites ever. The same thing with high-throughput satellites. I remember people said this will never work. Now it is the most profitable part of satellite communications.”

The thread connecting them, he argues, is simple: “Data. It’s meeting a terrestrial market that says, ‘Feed me. Feed me data.'”

Litteral sees elevated attention in the sector but not the retail frenzy that characterized past bubble conditions. For his firm, the discipline is accepting long aerospace development timelines and real execution risk in exchange for a differentiated position at the intersection of AI demand, space infrastructure, and the shifting politics of energy and data.

On timelines, there is more agreement than the debate might suggest. Shabtai sees micro data centers in orbit within three to five years. Eisele puts full-scale orbital AI compute in the five-to-10-year range. Litteral expects revenue-generating orbital data centers by the early 2030s. Mason puts small but useful clusters two to three years out and terrestrially competitive workloads closer to a decade. Karpf sees sovereign cloud as viable today, with the rest of the stack following if and when communications technology catches up.

None see the world’s appetite for AI going away, or ground-based AI data centers sustainable in the long term.

“We can’t keep up as it is today,” Eisele says of terrestrial AI infrastructure. “People are becoming more and more dependent on LLMs right now. I don’t think anybody wants to give it up anymore.”

Mason predicts that orbital data centers will be funded by hyperscale cloud providers, governments and defense/intel customers, and large commercial/sovereign customers with specific regulatory or latency needs—rather than by space companies alone.

The question isn’t whether data centers will eventually move into orbit. The physics, economics, and geopolitics all point in that direction. The question is sequencing — which workloads, which architectures, and which business models get there first.

Two points are clear: The enabling layers are being built right now — and the decisions about where to invest and what to prove will determine whether the orbital data center becomes the commercial space industry’s third great profit engine, or a very expensive lesson in the gap between physics and market reality. VS